Int. J. Financial Stud. 2023, 11(3), 101; https://doi.org/10.3390/ijfs11030101 - 07 Aug 2023

Abstract

News on the stock market contains positive or negative sentiments depending on whether the information provided is favorable or unfavorable to the stock market. This study aims to discover news sentiments and classify news according to its sentiments with the application of PhoBERT,

[...] Read more.

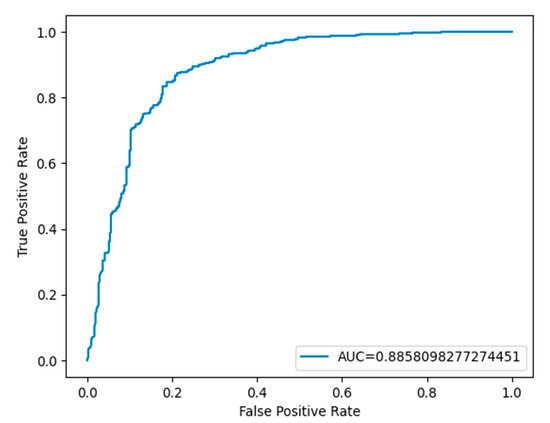

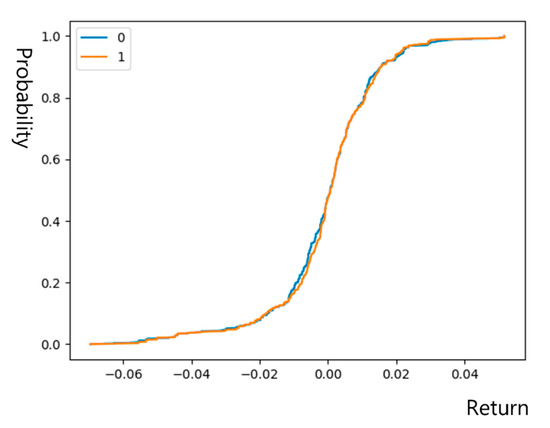

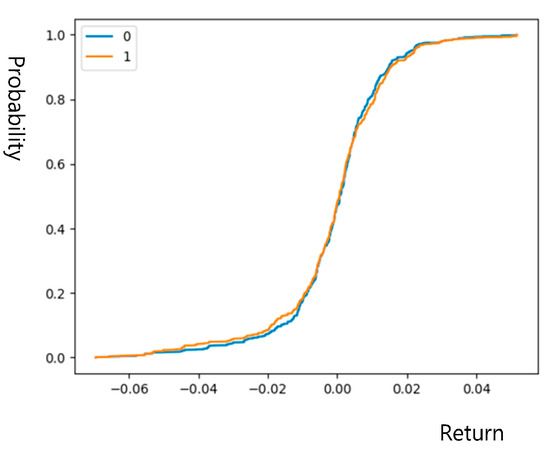

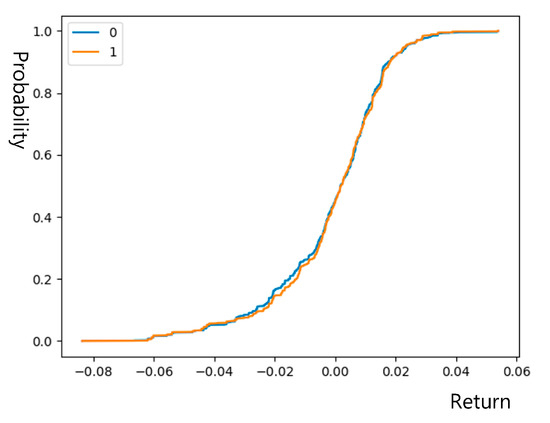

News on the stock market contains positive or negative sentiments depending on whether the information provided is favorable or unfavorable to the stock market. This study aims to discover news sentiments and classify news according to its sentiments with the application of PhoBERT, a Natural Language Processing model designed for the Vietnamese language. A collection of nearly 40,000 articles on financial and economic websites is used to train the model. After training, the model succeeds in assigning news to different classes of sentiments with an accuracy level of over 81%. The research also aims to investigate how investors are concerned with the daily news by testing the movements of the market before and after the news is released. The results of the analysis show that there is an insignificant difference in the stock price as a response to the news. However, negative news sentiments can alter the variance of market returns.

Full article

(This article belongs to the Special Issue Financial Econometrics and Machine Learning)

►

Show Figures

Figure 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}